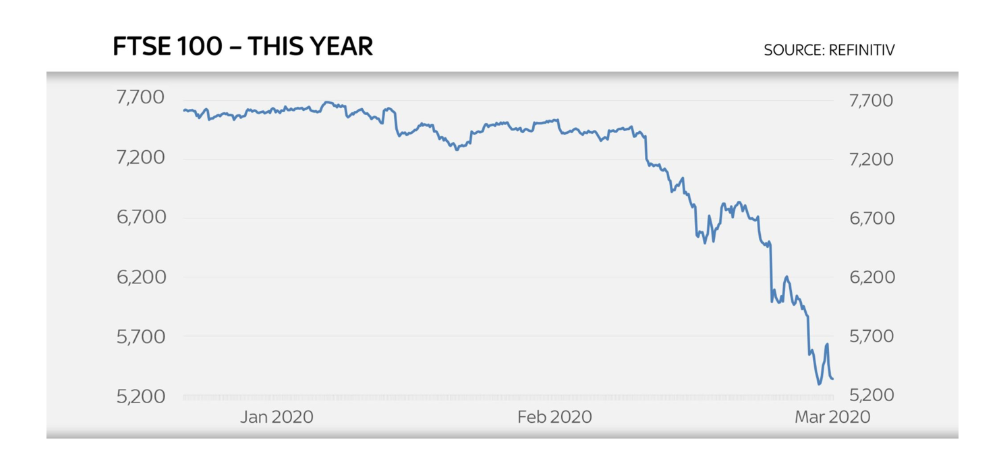

We’ve just seen one of the worst weeks in stock market history, with the FTSE100 ending on Friday 17 per cent down and billions of pounds wiped off British share values. This has been spurred on not by the fear of Covid-19 itself, but by the reaction to the virus: when sentiment switches from confidence to caution, panic can be self-reinforcing.

In response to the panic, the Bank of England slashed interest rates to 0.25 per cent; hours later, Chancellor Rishi Sunak used his first Budget to respond with a £30 billion stimulus package – the biggest giveaway of any Budget since 1992. In reality just £12bn of the £30bn is for the virus disruption: the rest is a debt-fuelled stimulus. But Covid eclipses all.

Below are seven graphs which sum up an extraordinary week of economic news:

FTSE 100 tumbles

There have been few weeks like this one…

(Source: Sky News)

Covid-19 hasn’t just stopped people and goods from crossing borders, but money too.

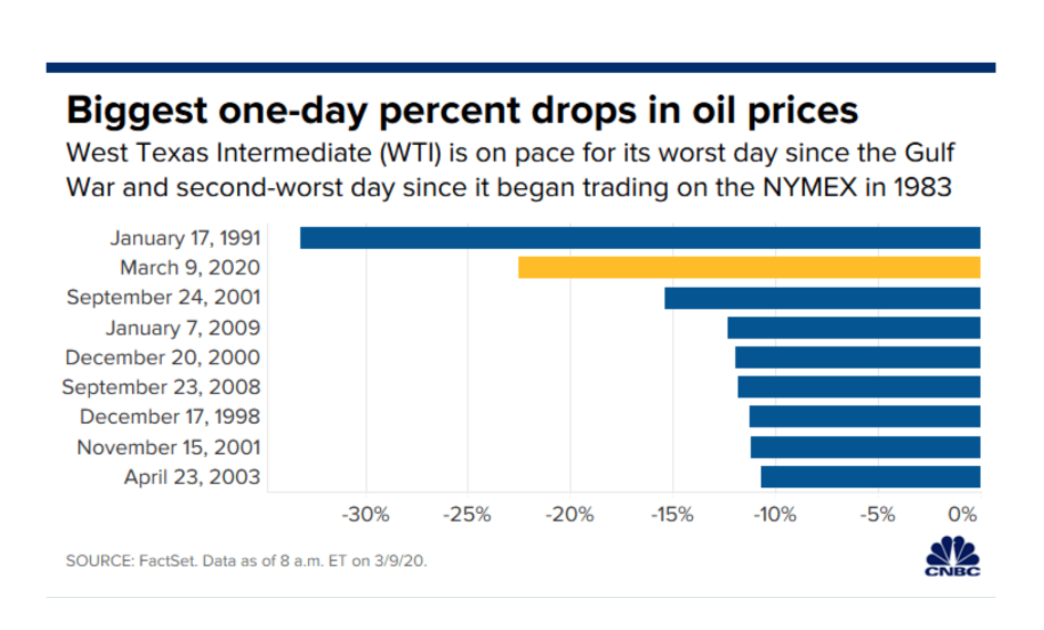

Oil prices plummet

Once, cheap oil would have made the stock markets boom – usually resulting in lower costs and more profits. But this time, low prices badly hit the US fracking industry, which is now so big that a knock to its fortunes can send shares plunging. This week’s dip isn’t simply due to Covid-19 worries, but the sudden oil war launched by Saudi Arabia against Russia, which has sunk princes to $30 per barrel.

The drop this week was the second-biggest one-day oil price shock in history. While the oil war rages on between MBS and Putin, it’s thought America’s shale gas industry could be the biggest loser:

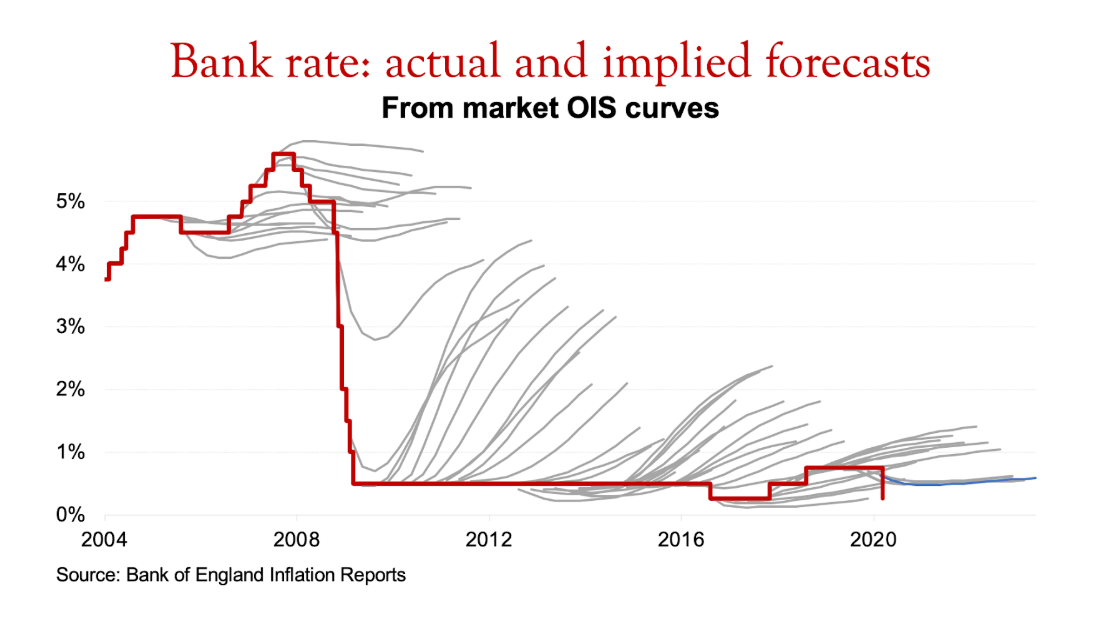

Bank of England slashes interest rates

The below graph shows the Bank of England base rate, now cut once again, and the gradually-declining market expectations for how that rate will recover. Slowly, the market has given up hope of ever getting back to normal interest rates.

Criticism has been levied at the BoE for slashing interest rates yet again, trying to stimulate spending at a time when business is going to struggle for customers – especially if the more serious public health measures being floated – like bans on mass gatherings and self-isolation for over 70s – are activated. And given that interest rates have been virtually extinguished since the crash, it’s unclear how much (if any) of the base rate cut will be passed down to consumers.

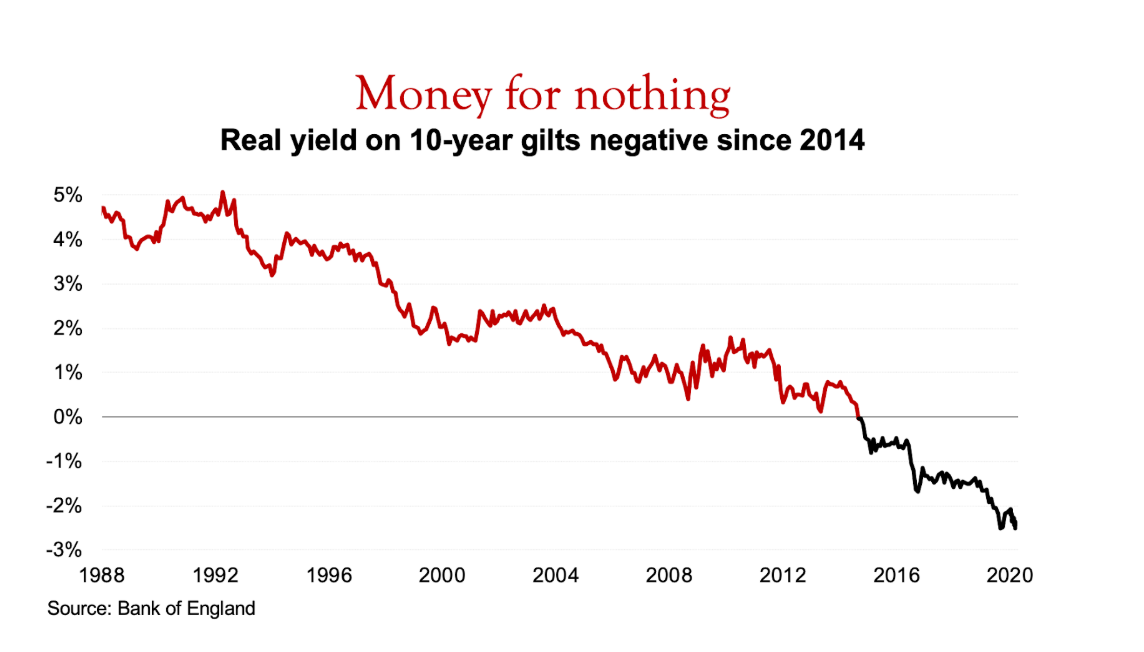

Negative real interest rates: a huge temptation for governments

As investors flee the stock market, they rush to lend money to governments – on the basis that it’s a safe investment, and they’re more likely to get their money back. This pushes down the rate of borrowing for governments (and comes at a time when central banks are already keeping the cost of borrowing nailed to the floor). We saw this this last week: the yield on both US Treasuries and British gilts plunged. There’s talk of US Treasury yields dropping to zero.

If you adjust for inflation, government interest rates are now actually negative. That is to say: investors are so nervous about losing money in the market, they’ll effectively pay the UK Government to protect their money, even if it means not getting their full return at the end. The Chancellor made this point in his Budget speech: surely it should be the amount of debt interest that counts, he says, not the actual debt. This raises a fascinating question: does the Conservative party believe in balanced budgets anymore? Or do they take a Krugmanite view that it’s time for ‘permanent stimulus’?

As the OBR chairman Robert Chote mentioned on the day of the Budget, this economic strategy has more similarities with a Gordon Brown Budget than it does with recent Tory leaders.

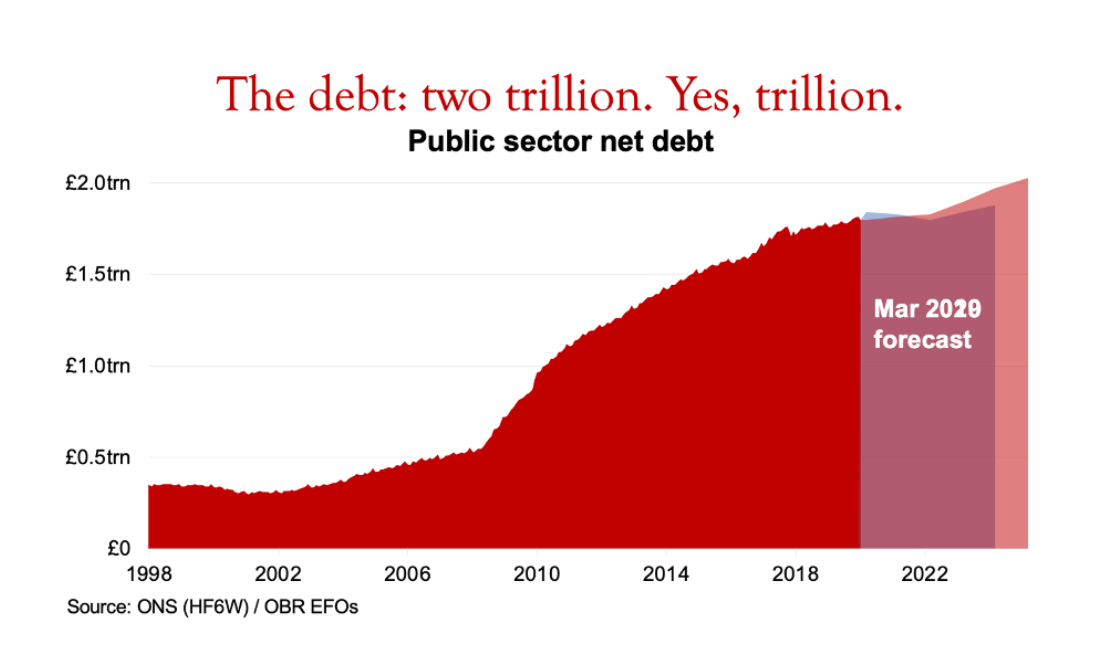

The £2 trillion debt pile

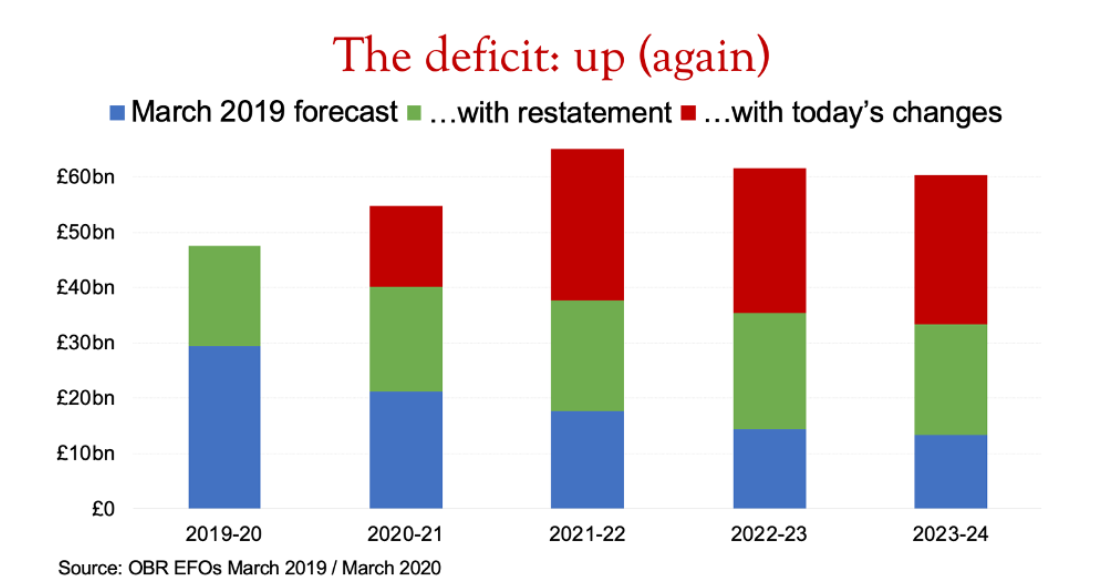

This logic – that the total amount of debt doesn’t really matter – leads to striking levels of national debt. After a decade of Tory Chancellors, the national debt is set to double from £1 trillion (when George Osborne took over) to £2 trillion (Sunak’s plan for 2023). The expected deficit in 2023/24 is now £60 billion, twice the £30 billion envisaged this time last year. It’s taxpayers, of course, who are on the hook for this debt if things take a turn for the worse. Once upon a time, the Tories came up with an easy way to simplify what an extreme burden this could turn out to be: thanks to “Gordon Brown’s debt” they said, every baby in Britain was born with £17,000 to pay back. On this basis, a child born now would be on the hook for £36,000 of debt. That was then. This is now. And the graph, below, is the future:

Global capital nosedives

A lesser reported story, but extremely timely from the Wall Street Journal. Covid-19 hasn’t just stopped people and goods from crossing borders, but money too.

I wrote a couple of weeks ago about how Covid-19 threatens the age of hyper-globalisation. For the foreseeable future at least, connectivity around the world is fraying.

Just as the wave of globalisation changed the world, its retraction too will have pretty far-reaching consequences. As will the Tory position on debt. As the saying goes, we live in interesting times.

Comments