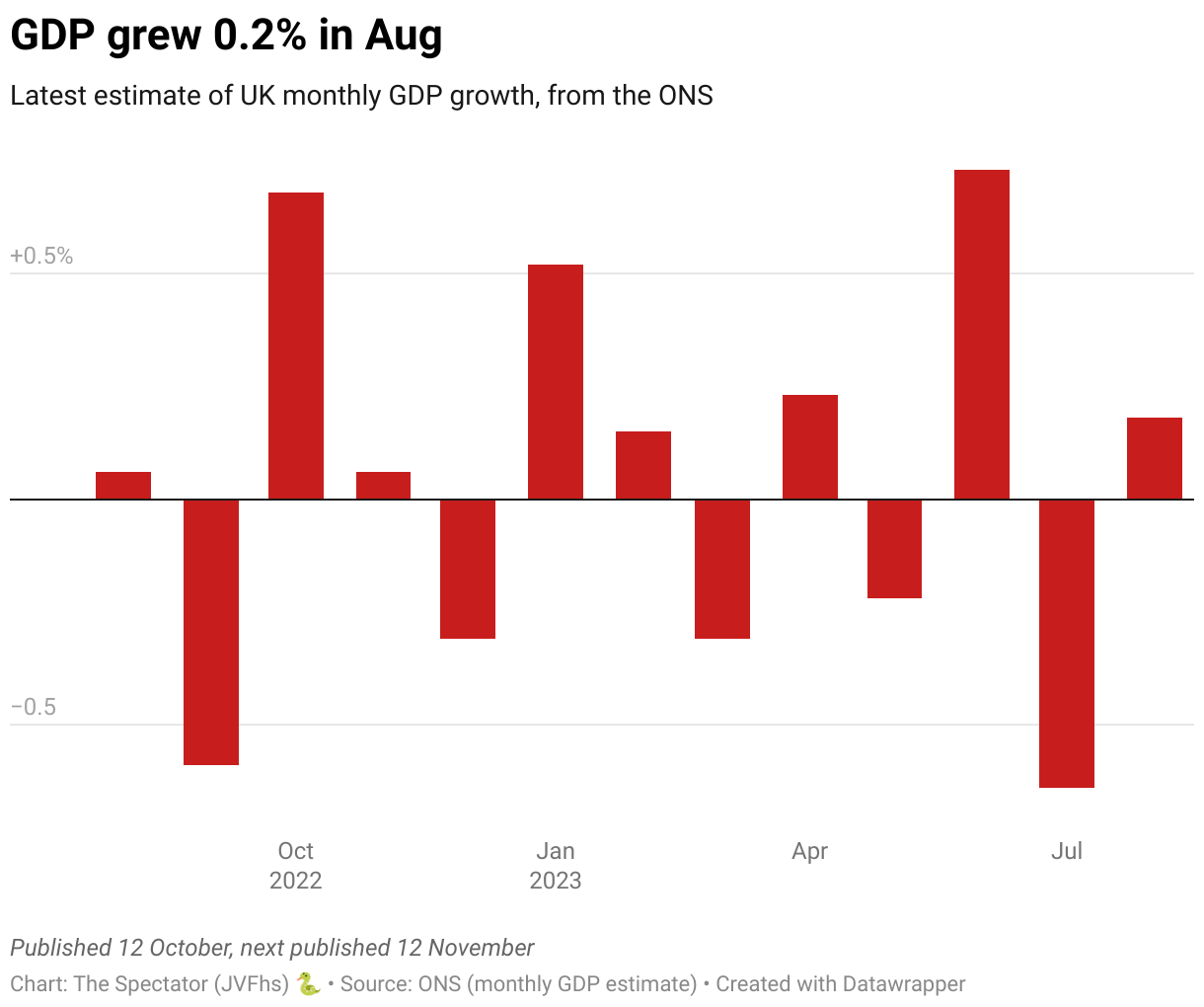

Britain has avoided recession – for now. This morning’s update from the Office for National Statistics (ONS) reveals that there was no overall GDP growth between October and December last year. The UK has swerved the technical definition of recession – two consecutive quarters of negative growth – in the least glamorous way possible. It is not a story of growth, but a story of stagnation, that has kept the dreaded label of ‘recession’ at bay.

The government will be relieved by the figures this morning: the fiscal tightening that Rishi Sunak and Jeremy Hunt felt they had to do last year to calm market jitters and get the public finances back in order always risked taking steam out of the economy and stifling growth. That risk still exists. But this morning the Chancellor is already noting that the economy ‘is more resilient than many feared’. Instead of having to describe the economy as one in recession last year, he can instead note that it was ‘the fastest growing economy in the G7′.

But no one should get too comfortable. The monthly figures for December last year, also released today, show that UK economic activity took a big hit, despite it being the first normal run-up to the holiday season in three years. The economy contracted by 0.5 per cent overall – 0.2 per cent worse than expected – with a 0.8 per cent dip in services (less health activity, in part due to strikes, is cited by the ONS as one of the leading causes for this fall).

Perhaps even more worryingly, December’s GDP fell by 0.1 per cent compared to the same month in 2021: a moment in time when the public was still isolating with Covid and voluntarily reducing activity as the Omicron wave hit the UK. For comparison, the ONS notes monthly GDP for November grew by 0.6 per cent between 2021 and 2022. So December’s GDP contraction is especially disappointing, when you consider the comparison between both the month and year before.

For now, the UK economy remains 0.5 per cent smaller than it was pre-Covid in February 2020. And these figures can still be revised. The ONS confirmed this morning that its monthly update for November remains ‘unrevised’ at 0.1 per cent growth. But the December figures won’t be confirmed until next month. If there is a downward revision, the UK still risks a formal recession.

Thankfully it seems the worst predictions for last year have been avoided. But forecasters are keeping an arm’s length between themselves and any kind of optimistic analysis this morning, as the real test of recession is yet to come.

The big forecasters, including the Office for Budget Responsibility and the Bank of England, are still expecting a recession this year – although predictions are becoming shorter and shallower with each update. Capital Economics (CE) notes that ‘avoiding a recession in 2023 will prove harder’, largely due to ‘the drags from high inflation and high interest rates.’

CE also notes that households and businesses are holding up well, as ‘the combination of the government’s support and households/businesses using their cash reserves has so far cushioned the blow from the fall in real incomes’. But these reserves are bound to dwindle, especially as the Energy Price Guarantee changes in April to cover far fewer people. Meanwhile the impact of inflation on people’s pay packets continues to inflict the cost-of-living squeeze. The latest labour market update from the ONS shows both total and regular pay down 2.6 per cent on the year in real terms, ‘among the largest falls in growth since comparable records began in 2001′.

This remains one of the big problems with the technical definition of recession: it is, of course, much better for the UK to have dodged a formal recession last year than to find itself in one. But that is no guarantee that people feel better off. With real wages taking such a hit, many will feel as though we’re in recession anyway. No growth in Q4 last year translates to fewer opportunities and less prosperity, which makes everyone feel poorer. And that’s before we get to the economic trials and tribulations 2023 has in store.

Comments