Britain is midway through a deep recession: of that there is no doubt. But what next? Oxford Economics has today been one of the first to offer an answer, predicting a V-shaped economic recovery (sharp economic downturn and sharp economic revival) and near-complete economic repair. It is, of course, a guess: all forecasts are. But it’s one worth looking into in a bit more detail. All published economic forecasts pre-Covid-19 (including those accompanying the Chancellor’s Budget last week) are defunct, so this is an early test – one that factors in the Government’s policy of ‘social distancing’ and the profound impact this has on business as usual.

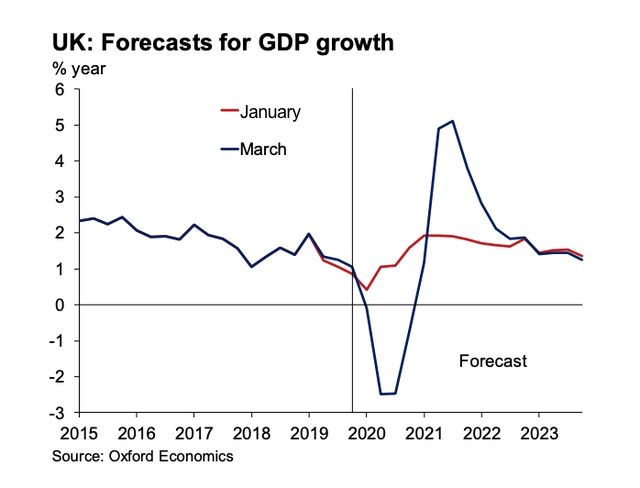

Oxford Economics has replaced its estimate of modest GDP growth of one per cent to a prediction of a fall of 1.4 per cent. Short-term growth has been slashed, now estimated to fall by three per cent in H1. And economic volatility will be with us for a while longer, as the combination of public health advice, working parents now looking after school-age kids full-time, and further hits to service sectors all take their toll on the economy.

Most pandemic modelling is about flu – but Covid-19 is not the flu

But unlike the 2007-08 crash, the economy here is crouching, on government instructions. Unlike during a normal downturn, we do not want people out and about, spending money and increasing economic activity; we want them out of restaurants, out of shops, keeping their distance from others. So the question is how high the economy is capable of standing later on, when things return to some level of normality. Oxford Economics says quite high: they forecast it will skyrocket with 3.7 per cent growth next year, returning to fairly familiar growth rates – albeit slightly higher – in 2022 and 2023.

Its base prediction: that between the monetary and fiscal stimulus on offer so far and historically low oil prices, Britain’s economy will have favourable conditions when it’s allowed to get up and running again.

But there is one big caveat: this modelling assumes that Covid-19, in historical terms anyway, is a short-lived phenomena which is tackled fairly quickly. This supposes that the Prime Minister’s estimates of ‘12 weeks’ to ‘turn the tide’ on the virus are largely correct, and we can crawl back towards normal economic activity in the second half of the year. In truth, no one knows how long this will last. This is an unprecedented situation, and a lot of the companies that will collapse during the crisis wont come back.

Oxford Economics notes that its previous studies regarding the impact of pandemics on the economy show that activity is ‘delayed’ rather than ‘destroyed’, which supports the V-curve narrative, that we can spring into action as soon as the immediate threat of the virus is eliminated. But just as this is not a normal recession, it is also not a normal pandemic. Most pandemic modelling is about flu (and it factors in a vaccine arriving in six months) but Covid-19 is not the flu, and a vaccine could be 18 months away. Nor do we know if Covid-19 will come back in a second or even third wave, as Spanish Flu did. In the worst-case scenario, it could mutate, making our public health response far more complex and expensive. There are many, many other variables.

But variables could work in our favour. A test to discover if a person has had Covid-19 (and should then be significantly more immune) looks to be delivered imminently: a test to see who has antibodies might release workers back into the economy more quickly.

So: still much uncertainty. But I suspect Oxford Economics will be the first of many forecasters to predict a V-shaped recovery.

Comments