Just how bad will the Covid economic hit be? Today’s figures for the first quarter of 2020 show Britain’s economy shrunk by two per cent, but that takes into account just a few days of lockdown (and suggests that the recession started some time before). The March figure is more like it: despite only formally being in lockdown for eight days in March, the UK economy contracted 5.8 per cent that month alone. As Capital Economics puts it ‘in just one month the economy has tumbled by as much as it did in the year and a half after the global financial crisis.’

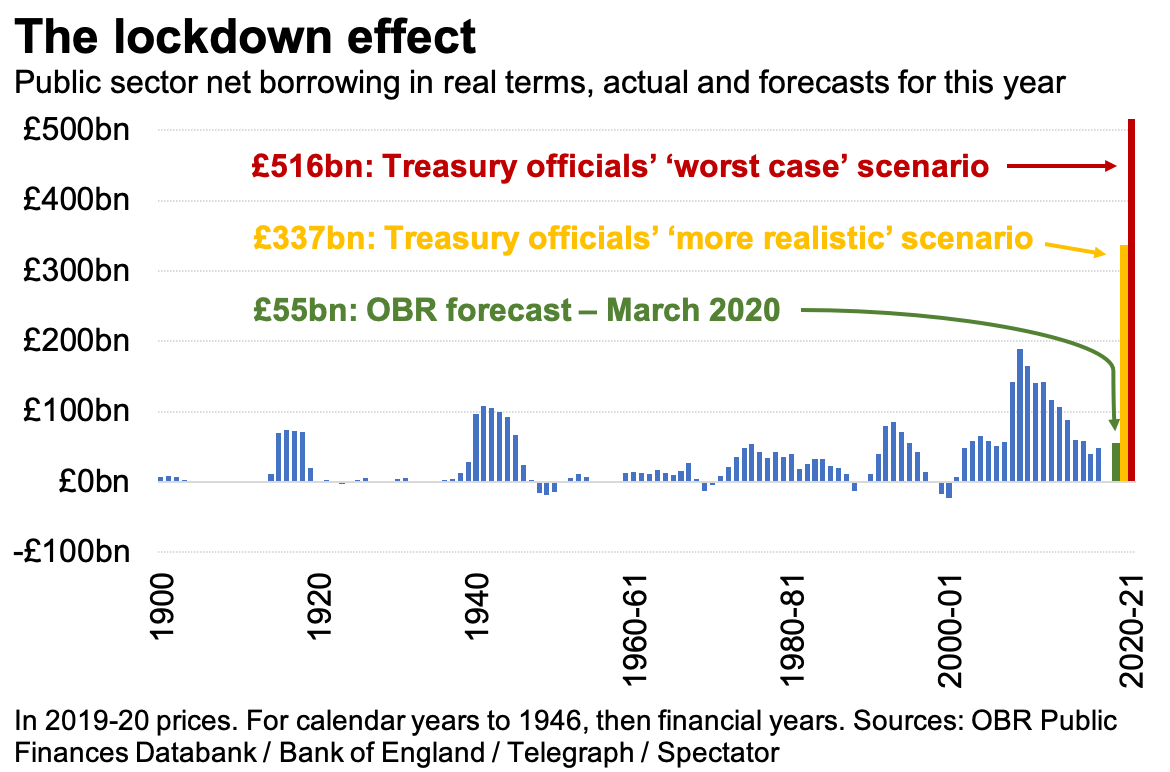

Yet some responses to today’s figures reveal a worrying degree of optimism about the future. The projections of a V-shaped recovery – quick downturn followed by sharp upturn – published by financial and monetary heavy hitters look as though they may have been too generous. If the UK was slow into lockdown, it’s coming out at a snail’s pace. This will be reflected in figures for the second quarter of the year and it will make for grim reading. Internal documents published by the Telegraph today reveal that the Government has been preparing for a U-shaped recovery. In short, that means a longer lag between the huge economic hit of Covid and the comeback. This won’t just have an impact on business recovery and employment rates, but could result in a £337bn budget deficit in 2020 alone.

And it could get worse. The Treasury’s worst-case scenario – an L-shaped recovery that results in lasting, unrecoverable damage to the economy – takes the deficit estimate up to £516bn. This projection doesn’t amount to a one-off spending spree, but the return of a huge structural deficit that even five years down the road could see the UK overspending by about as much as it was at the height of the financial crash.

From the Office for Budget Responsibility’s assessment, to the Bank of England, and now to the Treasury’s, the economic cost of Covid is only going up. This punctures a hole in some’s relatively relaxed assessment of the UK’s emergency measures, including the extension of the furloughing scheme until the end of October, often described as ‘wartime spending’.

That we can afford these colossal costs now rests on the assumption that interest rates stay at record ultra-lows, and that the inevitable increased costs of servicing this new debt can be managed with a growth agenda (or as the leaked documents suggest, by navigating the political minefields of tax rises and wage freezes). If the markets keep their faith in the UK, this may be manageable. If they don’t, today’s memo issues words of warning: ‘In a worst-case scenario, this could lead to a liquidity crisis and, ultimately, a sovereign debt crisis. A comparable UK scenario would be market conditions in 1976 ahead of the IMF loan when high and volatile inflation led to a loss of macro strategy credibility and a reluctance to hold UK debt.’

Either way, we will be living in far more economically uncertain and unstable times. There will be little room for manoeuvre. And as Covid has shown, in the most devastating way, you never know what’s coming round the corner.

Comments