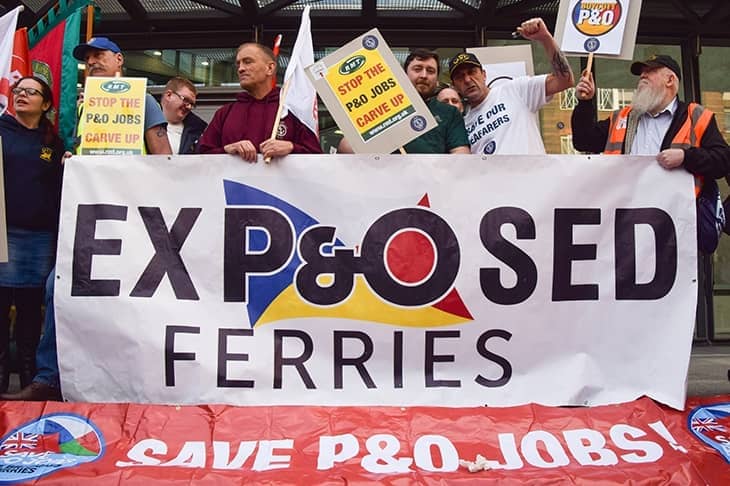

P & O once stood for ‘Peninsular and Oriental’, with pleasant connotations of sailings to Cadiz and Constantinople – but after the furious reaction to P&O Ferries’ sacking of 800 UK workers, to be replaced by cheaper overseas agency staff, you might think it stands for ‘Putin and his Oligarchs’.

With the mad Russian warmonger filling every headline, now is not a good time to turn yourself into a high-profile hate figure. With the pandemic barely over, now’s also not a good moment to be caught brutalising your workforce. But the man behind this sacking decision did all that in spades. He is Sultan Ahmed bin Sulayem, chairman of Dubai-based port operator and P&O Ferries owner DP World, and reported to have a private island and a hotline to Dubai’s ruling Al Maktoum family. In short, he’s the very essence of an Emirati oligarch – and no one anywhere is prepared to defend his company’s action.

But that leaves two headaches for the UK economy. First, the temporary suspension of P&O ferry services to Calais and Rotterdam is another disruption to our limping export trade following January’s introduction of the full gamut of post-Brexit red tape. Second, DP World runs shipping terminals at Southampton and London Gateway that are due to receive government funds as part of Rishi Sunak’s ‘freeport’ scheme, designed to make our external trade more efficient. But whatever the logic of working with such a sophisticated port operator, DP World’s tainted name makes that partnership toxic.

If there’s a moral to this story so far, it comes, I’m afraid, with a large dose of hindsight. When DP World bought P&O in 2006 for £3.9 billion, beating a bid from Singapore’s port authority, globalisation was rampant and this kind of inward investment was hailed as a vote of confidence in the UK. Now we’re in a different era of nationalism, protectionism, obstructed borders and security concerns on all fronts, the passage of so many strategic assets and businesses into foreign hands will be an increasing cause of regret and concern.

Shopkeeper needed

The auction of Boots by its American owner, Walgreens, has begun – with Blackburn-born petrol-station billionaires Mohsin and Zuber Issa, who bought Asda in 2020, entering the bidding in partnership with TDR Capital, a London private equity firm. The other contenders, Apollo and Sycamore Partners, are private equity players from the US.

When this sale was announced, I observed that the 2,200-store chain had done well to maintain its ‘hygienic [and] convenient’ place in our high streets despite recent changes of ownership — and that it would be best for Britain if Boots remained exactly the same. Recent experiences, however, forced me to revise that opinion.

Here’s one. In search of some prescription pills, I visited Boots’s big Longacre branch. The pharmacist said she had none but her computer said Tottenham Court Road had stock. She rang to check but they didn’t answer – and when I got there, the pharmacist said he had none, the computer was always wrong, and I should try Oxford Street. But the first Oxford Street branch had closed its dispensary and I had to try two more nearby before I struck lucky.

Throughout this two-hour tour, other customers were clamouring for lateral flow tests, but there were none. The impression was of a dysfunctional company and demoralised staff – despite a brand strong enough to make me keep looking for another Boots. And that tells me the chain needs hands-on shopkeepers in charge, not money-men looking for the next exit. The enterprising Issas look the least bad option.

Nuclear passion

I leave the country for a week (see below) and return to find Boris Johnson embracing with the passion he used to reserve for extra-curricular interests the energy agenda I’ve been advocating for years.

New North Sea oil and gas? Bring it on. New nuclear, to meet 25 per cent of UK energy needs by 2050? Yes please. I’m guessing the Prime Minister had glanced at the case made by EDF, the French energy giant, that properly costed nuclear energy works out cheaper than fashionable renewables because wind and solar require excess capacity and battery storage to compensate for periods of low output, whereas nuclear generation is constant. EDF estimates the saving to consumers if nuclear (rather than other low-carbon sources) provides 25 per cent of UK power at £4.8 billion a year or £179 per household.

All well and good, but only if investors such as Aviva and Legal & General – who attended a recent Downing Street meeting on this topic and crucially are not Chinese – back the Sizewell C nuclear project which could eventually power six million homes. Legislation now in parliament will offer nuclear investors more attractive returns, but what really matters to them, I suggest, is whether Johnson meant what he said this week or was just grabbing a headline to upstage Rishi Sunak’s spring statement – and whether this government and its successors will keep shilly-shallying on nuclear as all UK governments have done for the past 30 years.

Worth the trip

I’ve been back to France after a long interval, and loyal readers will want to know where I’ve been eating. My habit of peppering this column with restaurant tips originated from summer sojourns in the Dordogne at times when business issues seemed less urgent. But in today’s fear-filled world, is gastronomy too self-indulgent a topic? Or does it count as therapeutic relief? I’ll opt for the latter and mention one anti-inflationary offering: the €15 set lunch including wine and coffee at the unchanging Auberge de la Place in Cazals, Lot. It crossed my mind as I tucked in with gusto that the meal now cost the same as just seven litres of petrol: an odd change of relativities but a new meaning for the old Michelin exhortation vaut le detour.

Comments