Many CoffeeHousers will give a horse laugh to the idea of “green shoots” – especially the idea of Gordon Brown winning a fourth term because a grateful nation will thank him for a recovered economy. It’s a delusion, nothing surer, and the same one Callaghan and Major suffered from. In both cases, there were firm signs of an economic recovery – but the electorate never forgave the government which landed them in the mire. But is Britain recovering? We’ve seen a few developments lately which, given the fun and games elsewhere, have gone unnoticed. So here’s a catchup.

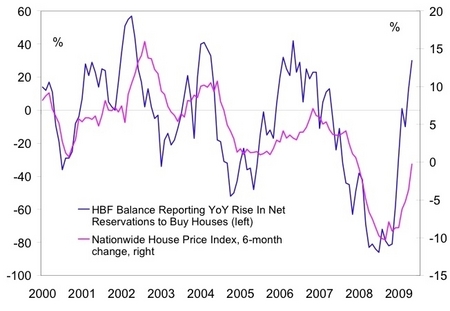

Pick up the financial pages, and you’ll find numerous stories of success: bonuses are back, the corporate debt market has recovered, house prices are moving. Take the Home Builder’s Federation survey – where it goes, house prices tend to follow. And it has shown the sharpest-ever rise in reservations to buy new houses. Confidence seems to be returning to the market (below):

Every recession is different, but not that different. The trajectory of the last two recessions suggest we should be bottoming out soon – perhaps now, in the current quarter (Jul-Aug-Sep period):

Unemployment lags economic growth by about nine months so will keep rising probably until election time. Every time Brown talks about green shoots, the Tories can reply simply: “in the real world, jobs are still being lost.”

But the flip side to this is the deficit. The Bank of England was supposed to use a third of its asset purchase facility to buy private sector assets – yet over 97% of the £150bn is being used to finance Brown’s misbehaviour by buying UK debt. Something like 0.7% of the cash has gone to private firms, of which half to foreign-owned ones like France Telecom and EON. It’s a deeply suspicious, inflationary scam. But that’s another story.

Inflation fears are most certainly back, and BoE will run out of justification to print cash (which it has been doing at about a staggering £1bn a day) and force Brown to rely on real investors with real money to buy his debt. Good luck to him. Foreign investors are dumping UK gilts, and have been for a while. They’re the ones in green, below, who Brown was relying on for some time.

So how will the Office for Debt Management – ie, Brown’s debt-mongers – find buyers for all these IOU notes when the BoE has turned off its printing press? The Treasury view is that UK debt/GDP ratio – at 55 percent in May – still remains beneath that of chronic debtor countries like Japan and Ireland, and that the markets only care about a country’s ability to repay. So it’s not the deficit they worry about, but the debt.

That’s one way of looking at it. Another way is to say that S&P has already turned ‘negative’ on Britain, that most analysts think we’re heading for 90 percent debt ratio and that no country on the planet with debt at that levels has a pristine credit rating. If people think the UK is heading for a downgrade, it’s enough to scare away international buyers – and perhaps the private UK ones, too. Perhaps Brown will make sure the nationalised banks siphon our savings into his debt. Or perhaps there will be a buyers’ strike and the Sword of Damocles will fall.

My point: we could well be starting a long, slow recovery. But when the BoE stops its helicopter money policy, Brown might face a fiscal crisis to replace the economic one.

Comments