There’s been much debate on these pages about the political implications of higher inflation. Ironically, this morning’s news of record food prices could relieve the pressure on the Bank of England Governor. His argument for caution when it comes to a rate rise is based on the claim that UK inflation is now being driven by events beyond the MPC’s control. Today’s figures reinforce that case, showing that global commodity prices remain a key driver of the rising cost of living in Britain’s households.

The same argument doesn’t really work for the Chancellor, whose remit isn’t just to keep headline inflation down, but also to help households cope with the kind of inflation we’re now seeing – whatever its cause. In fact, the changing ‘shape’ of inflation, and the shift in weighting towards food and fuel, makes life even more difficult for anyone trying to develop a political or policy response.

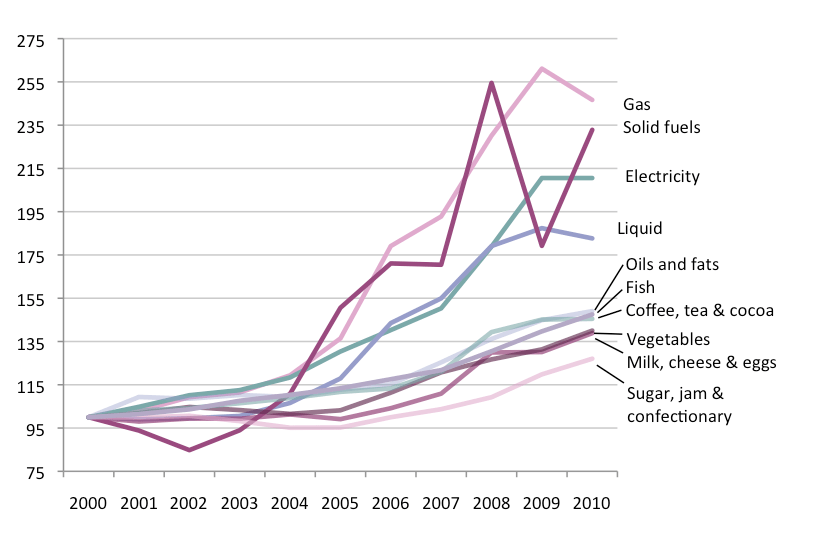

In this respect, two particularly worrying aspects of the new inflation emerge from a report we published at the Resolution Foundation last week. First, the big pressures on household budgets are now coming from categories of spending that are hard to avoid. The below chart shows the top ten categories of CPI inflation since 2005. It confirms what is often claimed – food and fuel have taken the front seat. If that is sustained over time, it will see necessities eat up a bigger share of household budgets. The share of income that feels genuinely discretionary or ‘disposable’ will fall. Life will feel more pressured.

Top ten subcategories of CPI inflation since 2005 (Index, 2000 = 100)

Second, the new inflation is driven by categories in which spend is much less evenly distributed across the population. While the share of spend on some categories like clothing or household goods

is fairly evenly spread across income groups, spend on food, housing and fuel is very uneven. On average, households on above average incomes spend around 11 per cent of their income on food and 11

per cent on housing, water and fuels. Low-to-middle income households spend 14 per cent and 17 per cent respectively.

Different spending patterns by income group: share of spend

The new inflation therefore falls more heavily on the least well-off, a point that’s been made on these pages before. And it’s also more volatile than it has been before. In the entire period from 1989 to 2006, the difference in the actual (CPI) inflation experienced by households on higher incomes and those on low-to-middle incomes was never greater than plus or minus 0.5 percent. In 2008, with inflation more heavily driven by those uneven categories of food and fuel, true CPI inflation was a whole one percentage point higher for households on low-to-middle income than for households on above average income.

When it comes to policy responses in this area, the public debate rarely gets beyond petrol duties and VAT. But the reality is that the government oversees a whole suite of policies that alter the profile of household living costs, and people’s ability to meet them. From the indexing of benefits to competition policy to specific support for work-related costs like childcare, much of this infrastructure was designed for different times. If recent trends continue, it’s going to need an overhaul.

James Plunkett is Secretary to Commission on Living Standards at the Resolution Foundation.

Comments