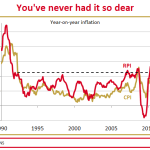

What you need to know ahead of tomorrow’s growth figures

By now, George Osborne will have seen tomorrow’s GDP figures and I suspect will be having a mid-afternoon whisky. Ed Balls will be warming up for his demands for a Plan B. “Austerity isn’t working,” he’ll say — and will doubtless tour TV studios with his usual bunch of dodgy assumptions which he hopes broadcasters won’t challenge. Here, as a counterweight, are a few facts and figures about austerity, how harsh it is, etc. — and the case for a Plan A+. 1. Where are the “deep, harsh” cuts? The Q2 GDP data will complete the economic picture for the first year of George Osborne’s time in the Treasury. But